》View SMM Aluminum Product Prices, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

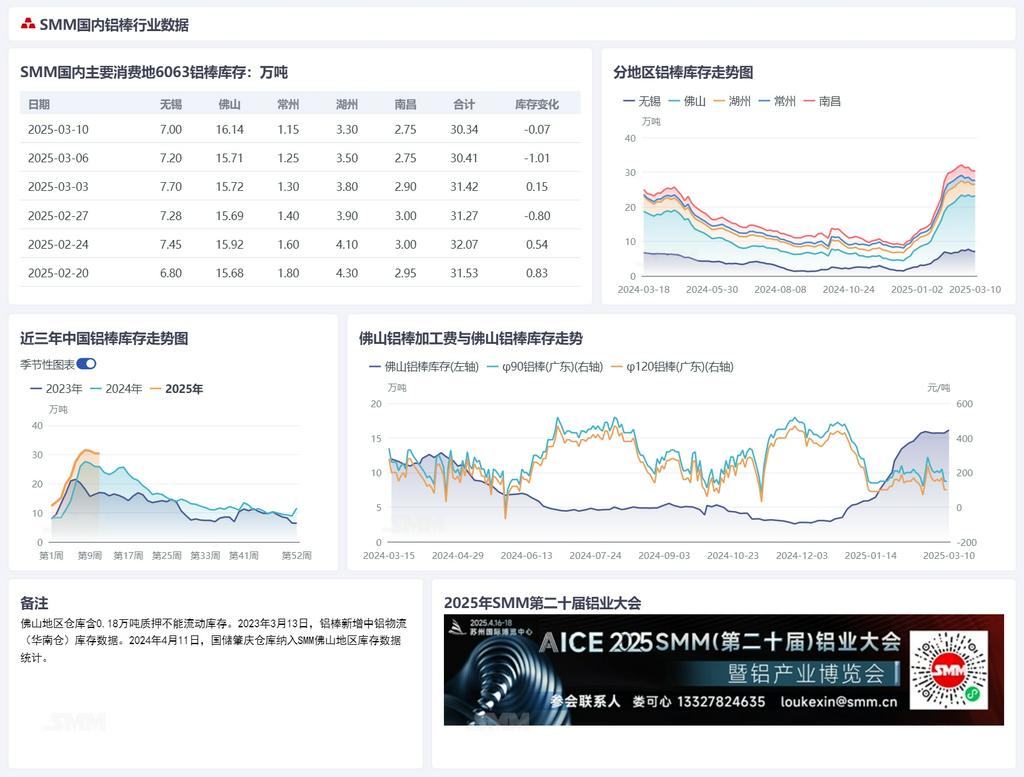

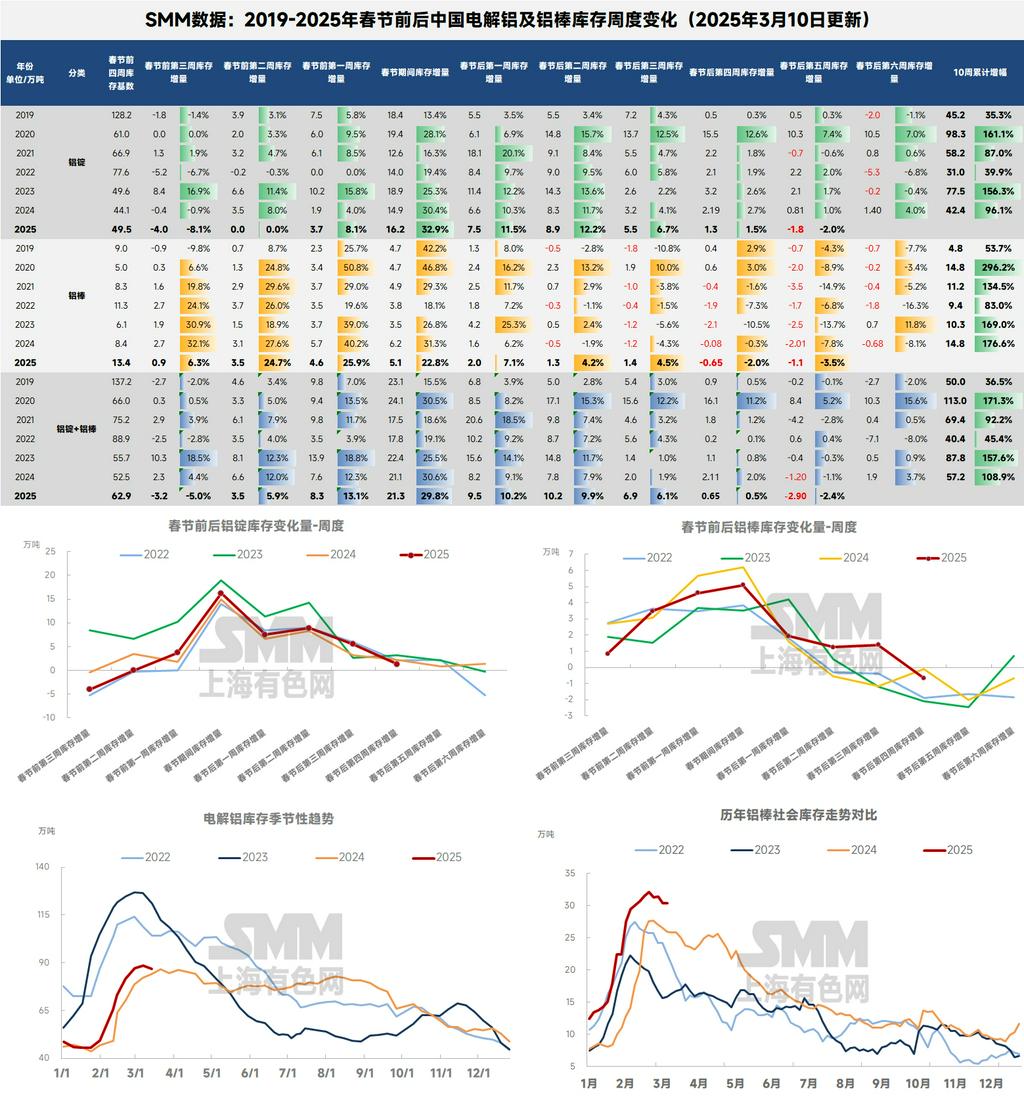

At the beginning of March, with the arrival of the traditional peak season of "Golden March and Silver April," coupled with the continuous consumption of upstream production site inventory, aluminum ingot and billet outflows from warehouses have continued to rebound over the past week. In-transit cargoes and weekend arrivals have also shown a declining trend. Supply and demand pressure has eased simultaneously, and domestic aluminum inventory has significantly improved, with a notable slowdown in inventory buildup over the past week. Recently, aluminum prices have stabilized above the 20,500 yuan mark after a high-level correction.According to Shanghai Metals Market (SMM) data, as of March 3, 2025, the total social inventory of domestic aluminum ingots and billets increased slightly by 6,000 mt to 1.2 million mt. Although inventory buildup in the first three weeks slightly exceeded the same period in previous years, it "hit the brakes" in the past week, showing early signs of a turning point in inventory at the beginning of March, with spot trades gradually becoming active.Specifically, inventory increased by 6,000 mt WoW (up 0.5%), and compared to the same period over the past seven years, it has entered a relatively ideal state.

On the eve of the traditional peak season of "Golden March and Silver April," domestic aluminum inventory finally showed a strong performance. Last week, the inventory buildup of domestic aluminum ingots slowed significantly, remaining flat compared to the previous Monday, effectively boosting market confidence. After the weekend, with the slowdown in aluminum ingot arrivals in major consumption areas and the steady increase in outflows from warehouses, as of March 3, 2025, SMM statistics showed that the domestic social inventory of aluminum ingots was 886,000 mt, with available inventory at 760,000 mt. Although inventory buildup increased by 13,000 mt compared to last Thursday, the pace of buildup was significantly slower compared to the same period over the past seven years, effectively boosting market confidence. Regarding aluminum ingot outflows, the outflows from major domestic consumption areas over the past week reached 128,300 mt, up 9,200 mt WoW.

SMM analysis indicates that based on the overall inventory buildup after the holiday, current aluminum market inventory remains slightly higher than the same period last year. Previously, inventory had successfully surpassed the post-holiday peak of 865,000 mt last year. However, the seasonal mismatch between supply elasticity release and demand recovery has not shown a significantly weaker-than-seasonal trend. The inventory peak in Q1 is expected to be around 900,000-950,000 mt. However, with the approach of March, the east China region has shown early signs of a destocking turning point, leading to a timely "brake" on mid-week aluminum ingot inventory buildup. Meanwhile, driven by the expected peak season of "Golden March and Silver April," downstream operating rates are recovering in an orderly manner, and in-transit cargoes in east and central China have shown a declining trend. SMM predicts that the first destocking period this year is likely to occur around the sixth week after the holiday (mid-March), similar to previous years. Moving forward, close monitoring of the intensity of work resumption, the release of in-transit cargoes, and the fulfillment of end-user orders will be necessary to confirm the timing of the inventory turning point and peak level.

Regarding aluminum billet inventory, according to the latest SMM data, as of March 3, 2025, the domestic social inventory of aluminum billets was 314,200 mt, up 1,500 mt compared to last Thursday. After the first post-holiday destocking occurred last Thursday, a slight inventory buildup was observed after the weekend due to concentrated arrivals, which is considered normal. The post-holiday destocking turning point for aluminum billets has shown early signs and is expected to be further validated within one to two weeks. Notably, the continuous recovery of downstream extrusion plant operating rates after the Lantern Festival has driven outflows from warehouses to rebound. Over the past week, outflows reached 58,600 mt (up 7,100 mt WoW), setting a new high for the year. Although some aluminum billet manufacturers may have adopted volume discounts, this still reflects the continuous release of end-user restocking demand to some extent.With the advancement of the traditional peak season of "Golden March and Silver April," coupled with the continuous recovery of downstream operating rates, the market is closely watching the actual support of consumption recovery strength for the destocking process.

On the demand side for aluminum billets, the operating rate of the domestic aluminum extrusion industry recorded 52.5% over the past week, up 1 percentage point WoW, continuing the mild post-holiday recovery trend.In terms of specific segments, the industrial extrusion sector maintained high prosperity, with leading enterprises sustaining operating rates above 75%. Among them, the trend of automotive lightweighting has driven a surge in extrusion demand, and new capacity in Jiangsu and Guangdong has ramped up smoothly. The PV extrusion sector has benefited from both policy and market advantages, with SMM reporting increased order volumes for leading enterprises. The construction extrusion sector showed clear stratification: leading enterprises quickly resumed work with sufficient orders from rail transit and municipal projects, while small and medium-sized enterprises focused on short-term projects such as residential renovations and finishing existing projects, maintaining low operating rates. Notably, the pace of transformation for construction extrusion enterprises has accelerated. According to SMM statistics, a few enterprises have shifted capacity toward high-end fields such as NEVs and 3C electronics. With the advancement of trade-in policies and the acceleration of new energy infrastructure, the proportion of industrial extrusion is expected to increase further. SMM will continue to monitor inventory trends, changes in downstream demand, and the impact of industry and regional policies.